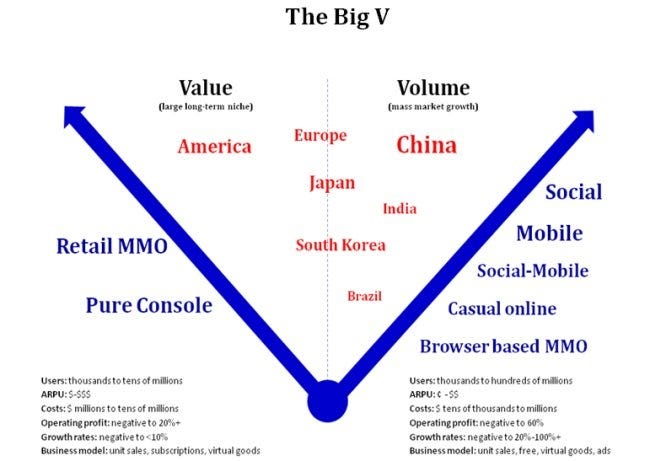

The Big V: The Great Games Market Split

Tim Merel of Digi-Capital looks at the market divide between value and volume

We are entering a world where the games market is fundamentally splitting in two, like the media market of a decade ago. Back then what we now call "old media" scoffed at "new media" upstarts for giving away content, bizarre business practices, and products and services which made no sense to the wise old birds. "They’ll destroy more value than they’ll create," was the mantra.

Well, welcome back to the future.

Today’s games market is fundamentally splitting into "Value" and "Volume" markets, both by sector and geography. The two-speed market this is creating may have more rapid and profound effects on the games market than it did on the media market, with meteoric rises for some and slow going for others.

Let’s start by defining what we mean by "Value" and "Volume".

Value

- Users: thousands to tens of millions

- ARPU (Average Revenue per User): $-$$$

- Costs: $ millions to tens of millions

- Operating profit: negative to 20%+

- Growth rates: negative to 10%

- Business model: unit sales, subscriptions, virtual goods

Volume

- Users: thousands to hundreds of millions

- ARPU: ¢ - $$

- Costs: $ tens of thousands to millions

- Operating profit: negative to 60%

- Growth rates: negative to 20%-100%+

- Business model: unit sales, free, virtual goods, ads

Please note that these are not hard and fast rules, so there will be exceptions (such as World of Warcraft in Retail MMO when we get to sectors). But as a way of thinking about how the games market is dividing and what it means, they are useful rules of thumb.

In terms of thinking about where each games market sectors fits, here's a starter:

Value sectors: Pure console, retail MMO.

Volume sectors: Social online, casual online, mobile, social-mobile, browser based MMO.

This categorisation may be relatively uncontroversial, but the geographic divide possibly less so. Please note that for geography we are discussing user markets, not necessarily developer markets. Companies from any geographic location can succeed in other geographic markets, such as Zynga (US) and Rovio (Finland) globally.

Value geography: North America.

Volume geographies: China, India, Brazil.

Mixed Value/Volume geographies: Europe, Japan, South Korea.

Put all that together, and you get the "Big V".

The eagle eyed will have spotted the small categorisations in brackets under Value (large long-term niche) and Volume (mass market growth) in the Big V chart above. If there is genuine controversy in this world view, it is probably here. So let’s explore.

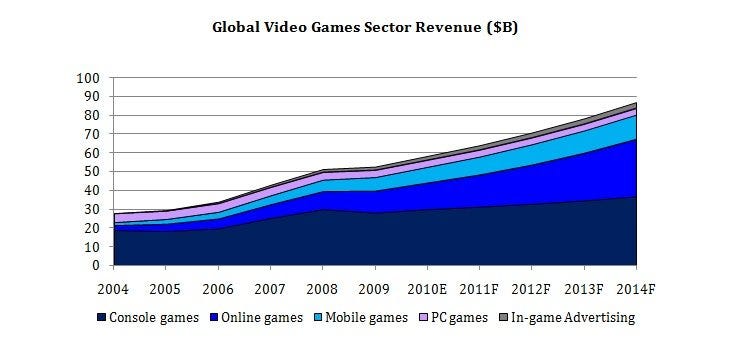

Our forecasts are that online and mobile games should grow total video games market size to $87 billion and take 50 per cent revenue share at $44 billion (18% CAGR 09-14F). The historically strong pure console sector is flat to down.

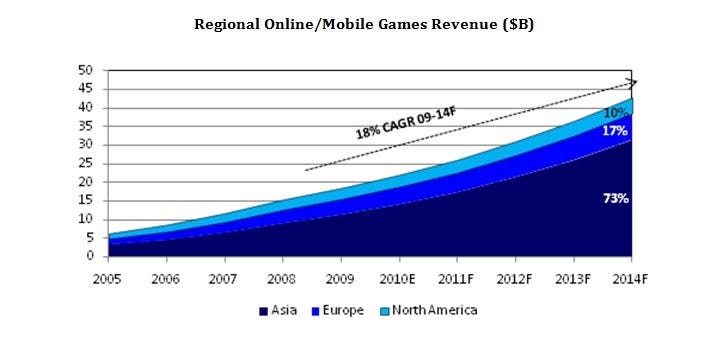

Our forecasts are that Asia Pacific and Europe should take 90 per cent revenue share for online and mobile games (China 49%, Europe 17%, Japan 14%, South Korea 11% in 2014F). North America remains important.

The drivers of this growing and changing world are socio-demographic and cultural, as well as technological. The most concrete statistics are socio-demographic, for which we’ll look at China as an example.

In 2010 China had 29 per cent internet penetration, with around 382 million users. So more Chinese internet users than the entire US population. China is forecast to reach 56 per cent internet penetration (754 million users) by 2015, or more than twice the US population, with the bulk of Chinese games played in internet cafes and on mobile phones. So while ARPU for gamers in China is much lower than America, the huge volumes enable Chinese online/mobile games companies to use incredibly efficient business models to deliver 50%-60% operating margins. To give a sense of scale, Tencent generates up to 20 million peak concurrent users, or roughly the population of Australia playing a Tencent game as you read these words.

China and the various online/mobile games sectors are the poster children for the Volume market, and fit the "mass market growth" description well.

For the Value side of the divide, the US and Console markets are good examples.

The US population is stable, so remains a large market. The Console market is flat to down, and despite recent and anticipated hardware launches we are unsure that this trend will change. Yet gamer ARPU in the US is much higher than China, and good Console titles still sell for high prices at retail (even if increasingly bought online or with digital downloads). So the US and the Console markets remain great games markets.

Yet compared to countries like China, the US is no longer the leading games Volume market in terms of gamer population. Even compared to Europe, the US is a smaller by volume. When it comes to the Console market, volumes, revenues and profits across the industry are generally trending down despite blockbusters like Call of Duty.

So in global terms these markets look like they may become large long-term niches. Still great places to operate, valuable, capable of producing great games companies and great games, but generally not on the same scale or with the same growth rates and profitability as the Volume markets. Some of these Value markets are trying to transform themselves into Volume markets, and they may succeed in doing so despite the challenges. As before, this is not absolute and there should be many exceptions.

Recent games investment, M&A and public company valuations (see the June transaction update of our Global Video Games Investment Review 2011 for the data) indicate that investors may be taking a similar view.

So what does this mean for your games company investment?

Whether you agree with this world view or not (and it’s certainly open to interpretation and discussion), the underlying trends are what they are. They can’t be ignored, so you may as well embrace them.

As a starting point, ask yourself some simple questions. Depending on your answers, you may start thinking differently about how to invest, plan and operate to take advantage of the brave new world.

- Users: are your games aiming at thousands, millions or hundreds of millions of users?

- ARPU: do you measure ARPU in cents or dollars?

- Costs: do you think of game development and user acquisition costs in thousands or millions, and do you have the right cost/revenue model for your markets?

- Operating profit: can your business be flexed to deliver super-profits?

- Growth rates: could your business deliver 20%-100%+ annual revenue growth?

- Business model: what revenue sources are most important for your games - unit sales, subscriptions, virtual goods (currency/items), ads?

- Geography: can your games operate across geographies and cultures, or are they domestically specific?

- Platforms: are your games platform specific, or can they operate across sectors?

- Value to Volume transition: what can you achieve in Value markets as they transform towards

- Volume, and how does that compare to what you can deliver in existing Volume markets?

- Scalability: are you building a genuine business platform with scale advantages, or a series of hits?

- Exit: can you become a "must-buy" for one of the major players in either Value or Volume markets, and what does that look like?

There are many more questions you could ask yourself, but deciding whether you are a Value or a Volume player (and keep in mind it is becoming increasingly difficult to be both) may have a profound impact on the future of your games business investment from valuation, investment, strategic and operational perspectives.

Welcome back to the future – it's going to be a lot of fun.

Tim Merel is Managing Director of Digi-Capital, the games investment bank focused on Europe, North America and Asia (China, Japan and South Korea). As well as its investment banking and venture partner work, Digi-Capital publishes its 2011 Global Video Games Investment Review, which focuses on the rise of online/mobile games, China and investment across sectors.