Stock Ticker: 2014 in Review

This year's winner and losers from the world's gaming stocks. Can you guess which company was the best investment of 2014?

It's been a tumultuous year for the games business in many respects, a fact that's been reflected on the world's stock exchanges as investors tried to place bets on the future of an industry that remains very much in flux. In this feature we'll take a look at who the real winners and losers of 2014 were in terms of stock prices; and, since those prices are based on investors' expectations of future performance, this should also give you some idea of which companies the world's markets are expecting to do great things in 2015 (although, as ever, it's worth cautioning that this isn't a crystal ball or a scrying pool, and markets get things drastically wrong on a regular basis, especially in volatile markets).

Let's start our tour of the world's gaming stocks with the biggest companies of all, the platform holders. Given the huge differences between the Japanese and US economies during 2014 (Japan back in recession and printing money like crazy to devalue its currency; the US on an upswing and the Dollar strengthening as it prepares to end its quantitative easing programme), I've opted not to graph companies from the two countries together for this feature, as it would be more misleading than informative, so let's kick off with the Japanese platform holders.

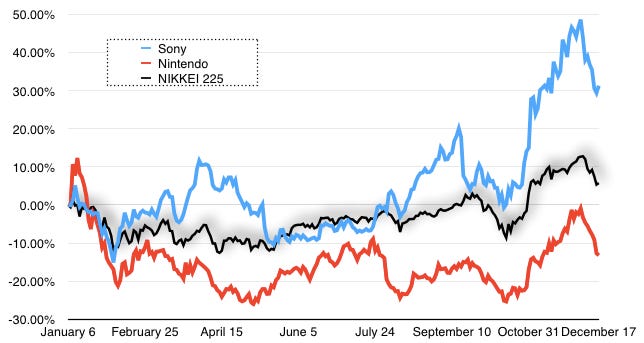

Despite a sharp fall at the end of the year - not least because of the embarrassing leak of internal emails, somewhat dubiously attributed to North Korean hackers - Sony has had a stellar year on the Tokyo Stock Exchange. It broadly tracked the modest rises on the exchange through the middle months of the year, bouncing higher as positive sentiment grew around the PS4, but really accelerated towards the end of the year as the scale of PlayStation's success and the extent of Sony's plans to build a more streamlined, profitable business around the PlayStation "pillar" became clear. This isn't a done deal as yet; Sony remains in trouble financially in many respects, and another reason for the recent downturn is that Microsoft has shown signs of starting to catch up to Sony's lead, if only in the US market. However, by and large 2014 has been just as good a year for Sony on the stock exchange as it was at retail.

"Nintendo, on the other hand, has had a fairly miserable time of it. Were the company a third-party publisher, Mario Kart, Smash Bros and Pokemon would have marked it out as one of the year's success stories"

Nintendo, on the other hand, has had a fairly miserable time of it. Were the company a third-party publisher, launching enormously successful new instalments of Mario Kart, Smash Bros and Pokemon, among various others, would have marked it out as one of the year's success stories; but it's not a third-party publisher (and, for what it's worth, I don't think it ought to be), and thus it lives or dies on the success of hardware. The 3DS is showing some signs of slowing, albeit remaining very healthy, and the Wii U remains extremely challenged, albeit a fair bit better off than it was this time last year. Still, the market is unimpressed; even with the hugely weaker Yen, which ought to prop up the company's financial results significantly, it has ended the year under performing the Nikkei 225 index of Japanese shares.

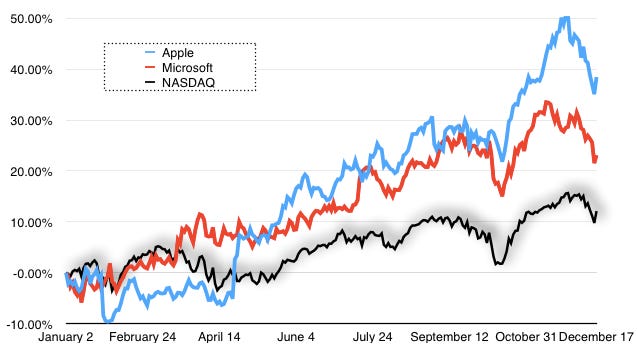

In the United States, it's a little tricky to track the performance of platform holders from a purely gaming perspective. I'm counting Apple as a platform holder simply because iOS is such an important platform right now, and unlike Android its success can be tracked within a single stock (Android is vastly more complex, as it's deeply entangled not only with Google but with various hardware manufacturers in different territories). Both Apple and Microsoft, however, do not have games as a primary business even to the extent that Sony does, so I'd caution against reading too much into the success both companies have enjoyed this year.

What a success it has been, though! Apple, already an extraordinary stock market success story, reached a new all-time high back in November, while Microsoft has bumped up against 14-year highs throughout the latter part of the year. For Apple, that's primarily down to the success of the iPhone 6, whose sales have confounded analyst pessimism; for Microsoft, much of this year's boost is down to continued enthusiasm for the direction being taken by CEO Satya Nadella, and especially the company's Azure cloud computing product, which is now second only to Google in this rapidly growing space. What that means for Xbox is tough to say; the company can certainly afford to keep subsidising the console space if it needs to, but with Surface being (quite sensibly) refocused on a high-performance niche and Windows Phone seemingly slowing to a halt, Xbox does look increasingly isolated in a company whose focus on consumer products is at an all-time low.

For the purposes of this feature, I've divided up publishers in the USA and Japan into two categories - "traditional" and "mobile" - but I should say at the outset that those category lines are more blurred with every passing month. A new kind of categorisation will probably be required by the time 2015 comes to a close, but for now I'll continue with the old one, while noting its obvious flaws.

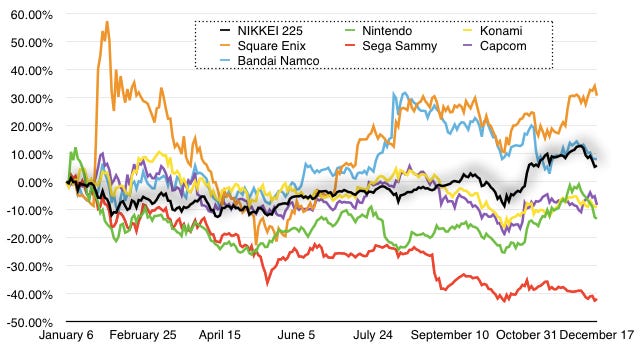

Among the traditional publishing sector in Japan, there's really only been one winner and one significant loser, with everyone else clustered in the middle. Square Enix is the year's success story, comfortably outperforming the rising Nikkei index; the huge bump in its performance at the start of the year is generally attributed to the success of the first Dragon Quest game to be launched exclusively as a mobile title, demonstrating the company's continuing commitment to (and success at) transitioning part of its business to mobile platforms. Along with strong fundamentals from other parts of the business - notably Final Fantasy XIV: A Realm Reborn, which stands out as arguably gaming's greatest example of pulling victory from the already-chewing jaws of defeat - the majority of Square Enix' stock gains this year are down to great execution on mobile titles.

"At the other end of the spectrum you've got Sega Sammy, which had a disastrous 2014 - almost entirely reversing gains it made throughout 2013"

At the other end of the spectrum you've got Sega Sammy, which had a disastrous 2014 - almost entirely reversing gains it made throughout 2013. That timing actually suggests the underlying reason for the problems. In 2013 there was strong speculation that the Japanese government would pass a bill legalising Macau-style casinos in certain locations in Japan, a trade Sega Sammy would have expected to profit from handsomely - most of the company's business, these days, comes from pachinko and pachislot (legally not considered to be gambling, although given how many players end up deeply in debt to organised crime rings, the reality is very apparent), so properly legalised casino games would have been a major boost. In the latter half of this year, however, the proposed bill has been watered down over and over again before finally being shelved entirely. Of course, the lack of very many bright spots in Sega's gaming catalogue can't be helping things either.

As for the publishers in the middle, there's not a lot to say; Bandai Namco, buoyed by the huge success of Yokai Watch (look out for that being very, very big in western territories in 2015), had a pretty solid year, while Konami, Capcom and (as previously mentioned) Nintendo had an unremarkable time of it, with the former pair lacking much in the way of substantial software launches or announcements to pique the market's interest. Were it not for the declining value of the Yen, which should help their financial results, both firms would probably be looking a lot less impressive; as it is they're just lacklustre.

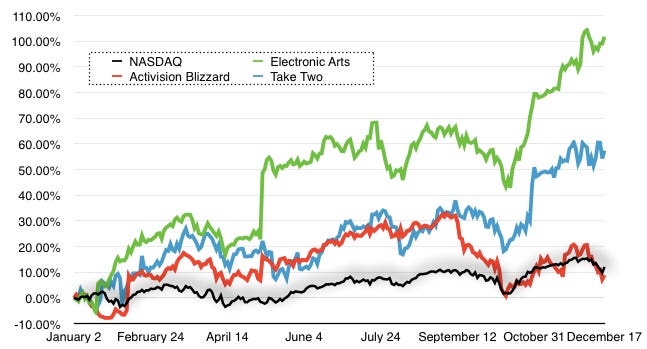

Turning to the United States, there's really only one question to ask; who has shares in Electronic Arts? If the answer is "me", then congratulations; the US publisher was the top performing games stock of 2014 by a very significant margin. It's doubled in value over the course of the year, thanks to a combination of the fruit being borne by planning set in motion by former CEO John Riccitiello, and the rock-solid execution of new CEO Andrew Wilson. Whether this momentum can be continued for another year is a tough question; much will probably depend on how Battlefield Hardlines performs, since that's the company's next roll of the dice at creating a really world-class "event" franchise on a par with something like Call of Duty. Even if it doesn't break out to that extent, though, just continuing to build momentum behind Battlefield will probably satisfy many investors who are impressed at EA's ability to keep inventing new franchises and, by and large, to update those franchises without milking them to death.

At the other end of the spectrum, Activision had a very mediocre year in stock market terms. The launch of Destiny was a strong point, as was the continued success of Skylanders in the kids' market, but investors seem to be cool on Destiny's much-vaunted "ten year plan" (I suspect that many of them saw Destiny as a new World of Warcraft, not a new annual franchise, and are a bit disappointed to see that it's more like the latter than the former; given that many gamers seem to have had the same misapprehension, it's hard to blame them for this). Moreover, Call of Duty: Advanced Warfare proved the thesis that this franchise is on the wane - it still sold tons of copies, of course, but even with Hollywood star power attached this time, the game's steady decline in sales continues. Modern Warfare 3 remains the high point; Advanced Warfare's sales are only around half of its exalted predecessor.

Take Two, incidentally, also had a great year - but what's perhaps even more impressive is that it's the company's third great year in a row, continuing a steady rise in share value that started back in 2011. There's no single game to which I'd attribute that rise - although the sharp uptick in Autumn is partially due to macroeconomic factors and partially down to the "second bite at the cherry" offered by GTAV's launch on new-generation systems. Rather, it seems that investors are simply impressed with the company's progress and the standard of its current management, and perhaps starting to get over the long-standing fear that should a GTA instalment ever fail to impress, it would bring Take Two down with it.

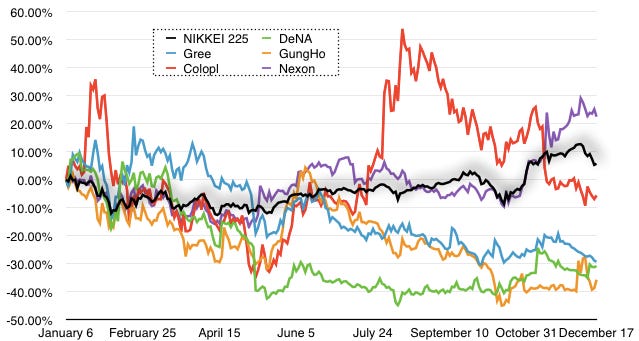

Crossing the Pacific Ocean again, we can take a look at how Japan's mobile publishers fared during 2014. The first thing of note about this graph is simply how busy it is; even having left out a couple of smaller firms (and one major one, CyberAgent, whom I'm not convinced is game-focused enough to justify inclusion, though I'd be happy to hear arguments to the contrary), there are five genuinely major mobile publishers listed in Japan right now.

The other notable thing here is just how volatile this market remains. There is a sense that after the initial burst of excitement around mobile gaming, investors are now running a little scared of the huge risk profile of stocks in this sector; that might explain why some game publishers are seeing their stocks rise, as an investor who wants to get into games right now is likely to see EA or Take Two as a much safer bet than a mobile publisher. I mean, look at this Japanese graph. DeNA and Gree, the original pair of Japanese mobile giants, both had pretty miserable years - and with both of them continuing to face difficulty in expanding effectively overseas along with intense competition at home, not helped by their continuing reliance on browser-type games rather than smartphone applications, the reality is that neither of them are very well positioned for 2015 either.

"Yet the worst performer of the year is neither of them; it's GungHo, publisher of Puzzle & Dragons and now parent company to SuperCell, of Clash of Clans and Hay Day fame"

Yet the worst performer of the year is neither of them; it's GungHo, publisher of Puzzle & Dragons and now parent company to SuperCell, of Clash of Clans and Hay Day fame. GungHo had some positive spots throughout the year, especially thanks to overseas performance for Puzzle & Dragons, but overall it's facing a market hammering for failing to come up with anything new that lives up to the success of P&D. It lost the top spot in the Japanese iOS charts recently, and suddenly GungHo's crown is broken and throne is stolen. It's a very tough, very volatile market, but that also creates opportunities for success; relative newcomer Colopl is a prolific publisher/developer that enjoyed a huge spike in popularity for its White Cat Story games this year, and has been building up an impressive portfolio of games in the iOS top-grossing charts. It doesn't have a Puzzle & Dragons on its hands, but a solid portfolio of mid-performing games may be a more sustainable approach.

Finally, there's the best performer on the chart (stealing the crown at the last minute from Colopl) - a bit of an oddity, the Korean company Nexon. Nexon all but invented the free-to-play model in South Korea, but it's listed on the Tokyo Stock Exchange and thus earns its place on this chart. It did have a solid 2014 in financial terms, but its last-minute spurt in value was more to do with currency than company performance, with the weak Yen making its Korean earnings look much better on its bottom line.

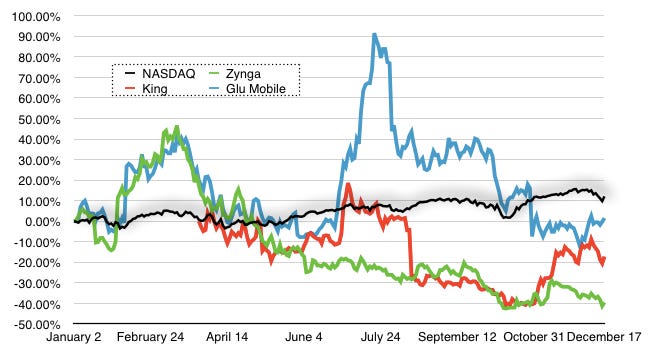

Back to the USA one last time, then, for a look at the major exchange-listed mobile publishers there. Again, volatility is the name of the game here. King, which listed in April, had a genuine cultural phenomenon on its hands with Candy Crush Saga, but like GungHo, it has failed to demonstrate its ability to repeat that success and has underperformed the NASDAQ since its IPO. Zynga, too, continues to disappoint; there's much talk of green shoots appearing under the new leadership of former Xbox boss Don Mattrick, but the company's continuing decline in 2014 suggests that the markets are taking such talk with a pinch of salt.

Glu Mobile is a publisher people often forget, but has been stock market listed for vastly longer than the other two. This year it saw an enormous spike in valuation thanks to the success of its Kim Kardashian licensed game; as is always the case with valuation spikes based on a single game, this was a bit of a flash in the pan, but if Glu can show that it's learned how to utilise mainstream brands effectively on an ongoing basis rather than just having one break-out success, investors are likely to take a strong interest in the stock in 2015.

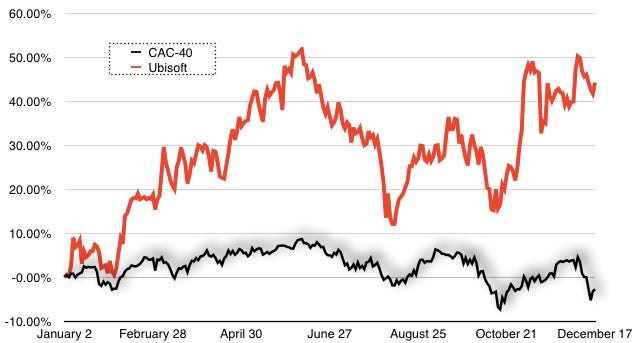

Last but not least, a publisher that is beyond compare; no, literally, there's no other publisher I can compared to Ubisoft, because every other decent-sized, market-listed publisher in Europe is long-gone (the final one to fall being the UK's Eidos, absorbed by Square Enix). Thus our only benchmark for Ubisoft's success is the company's local stock index, the Parisian stock exchange's CAC-40 index. (For what it's worth, if I did cheat and include Ubisoft with the US publishers, it would come in just below Take Two in the chart, albeit after a much bumpier year overall).

It has been a bumpy year for Ubisoft; Watch_Dogs didn't get the critical response the company wanted, and then there was the drubbing over Assassin's Creed Unity being released in a very unfinished state. Overall, though, the company has been an excellent performer on the Parisian exchange, continuing a steady climb in its value that started all the way back in late 2011. In many regards its climb mirrors Take Two's, though Ubi's has been significantly steeper; it's more than trebled in value since late 2011, compared to a more modest doubling in value for Take Two. It seems reasonable to speculate that investors see either Take Two or Ubisoft, both of which survived the incredibly tough transitions of the past decade in rude health, as being likely to continue to grow - doubly so should one of the giants, most likely Activision, stumble in some way. Investors like stocks that have room for growth, and both Ubisoft and Take Two have showed that in a big way. Whether either firm can keep that momentum going throughout 2015 will be interesting to see; from Ubisoft's perspective, probably the most critical question for 2015 is whether the Assassin's Creed franchise remains intact, and whether Watch_Dogs can be reinvented to more acclaim in its inevitable sequel.