Activision's New Deal: The Good and the Bad

[a]list daily examines the details of the buyout from Vivendi and what it means for Activision's future

The financial transaction involving Activision last week was massive and complex, which led to confusion in the media reporting on the event. "Activision goes independent" was part of many headlines, perhaps leading to an impression that Activision is no longer a public company. The exact opposite is true - Activision is more of a public company than before. The deal leaves Activision in control of its own future at the cost of adding a sizable amount of debt. How exactly has Activison changed, and how might this affect the future of the company?

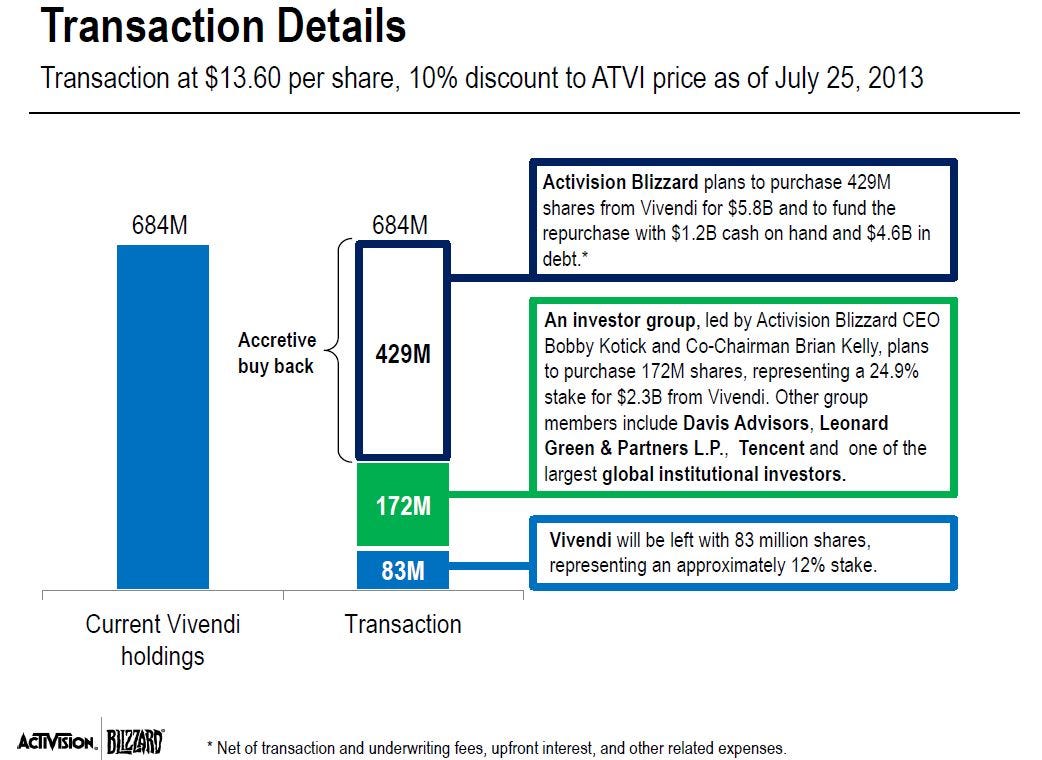

The deal itself has been under negotiation for months, and in the offing since the merger of Activision with Vivendi's games unit (most importantly Blizzard Entertainment) back in 2008. The merger at that time left Vivendi with 61 percent ownership of Activision-Blizzard, with the remaining 39 percent of shares held by the public. The catalyst for the current buyout was the expiration of a clause in the merger agreement that required Activison directors to approve any debt greater than $400 million, preventing Vivendi from taking Activision's cash or borrowing against the company.

Vivendi is seeking cash because it has a massive debt problem, owing more than $15 billion, and it wants to reduce that debt. Unable to find a buyer for Activision in the last year, Vivendi has accepted the deal put forth by an investment group led by Activision CEO Bobby Kotick and chairman Brian Kelly. Here's how the deal works: Activision is borrowing $4.75 billion from banks and using $1.2 billion of its own cash, along with $2.3 billion from an investment group, to reduce Viviendi's share of Activision to 12 percent. The investment group will own 24.9 percent of Activision, while 63.1 percent will now be owned by the public.

There are several good things about the deal, especially from the view of Activision's leadership. The deal puts the complete control of Activision in the hands of its board of directors. Shareholders have seen a good increase in the value of their shares. Importantly, the deal still left Activision with substantial cash, and a manageable debt load that's roughly equal to about four years of profits (at the current profit levels). On the negative side, the cash on hand is mostly overseas (some $2.6 billion out of about $3 billion) which would incur substantial taxes were Activision to repatriate it. The company will only have about $400 million in US cash handy when the deal closes.

It's the longer term picture for Activision that's murkier. The deal weakens Activision's ability to acquire new companies or to substantially invest in major new areas. A deal for Take-Two, say, would be more difficult now since Activision would have to incur more debt. The debt service shouldn't be a problem if Activision continues to generate the same sort of profits it has for the past several years, but there are signs that may be changing.

Read the rest of the analysis, including the dangers ahead, on the [a] list daily.