PC trumps mobile, console in booming $61bn digital games market

SuperData's Joost van Dreunen looks back at 2015's top digital earners and finds that PC is an undervalued platform

In 2015 the worldwide market for digital games totaled $61 billion across platforms, up 8 percent year-over-year. The largest category in terms of dollar sales was mobile, earning $25.8 billion and up double digits (10 percent) from the year before. Sales figures point toward a shift in the industry as more consumers have adopted digitally distributed games and free-to-play. However, not all segments were posting positive numbers, as social games remained flat (-0.8 percent) and subscription-based gaming continued on its downward spiral (-4 percent).

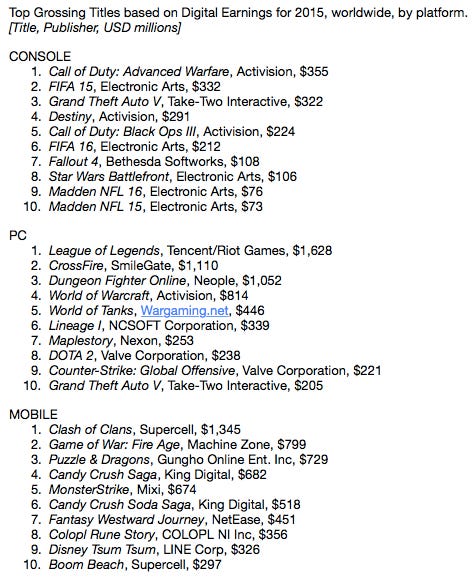

Based on their earnings in the top 10, last year's highest-grossing publishers were Activision ($2.9 billion), Supercell ($1.64 billion) and Tencent ($1.62 billion). Activision controlled six of the 30 top spots across platforms, including the titles that came under its ownership following the acquisition of King Digital late last year. Supercell takes the number two position overall with $1.6 billion in earnings across its titles in the top 10. And China's titan Tencent follows as a close third, based on its dominance in the PC market with its wildly successful League of Legends, earning $1.6 billion, or roughly seven times more than its closest competitor, Dota 2 (Valve), which earned $238 million in 2015. Despite claiming five of the top spots on console, Electronic Arts lacks a strong position in digital PC and mobile, earning it gross revenues of $798 million.

Digital console is relatively small and has high barriers to entry.

Following a stellar holiday season for the games industry, total sales reached a record high in 2015. Sales of digital console games showed the biggest jump and were up 34 percent, despite being one of the smaller categories at $4 billion annually. The market for digital console follows the traditional market for game publishing much more closely than any other category. The biggest publishers on console are Activision and Electronic Arts, with combined earnings in the top ten of $870 million and $798 million, respectively. EA's approach of publishing licensed titles claimed no less than five of the top slots on console. The only new franchise in 2015 to reach the top ten was Destiny, earning $291 million. It's no surprise then that the top 10 digital console titles claimed over half of worldwide revenues in 2015. By comparison, the top mobile titles accounted for 25 percent and PC for 20 percent in their respective segments.

PC is an undervalued platform.

Succinctly speaking, the top 10 PC games earn more than the top 10 mobile games. Contrary to the amount of attention that is generally paid to mobile gaming, total revenues from the PC gaming market is larger ($32 billion) than that of mobile ($25 billion). Or, sliced differently: the combined earnings of digital PC games for the top titles came in higher, totaling $6.3 billion in sales compared to $6.18 billion for mobile. The biggest PC segments are free-to-play MMOs ($17 billion) and social network-based gaming ($8 billion).

"The top game publishers are becoming so large that they can no longer sustain their growth by simply publishing more titles and claiming more market share in games"

The top titles are League of Legends ($1.6 billion), CrossFire ($1.11 billion), and Dungeon Fighter Online ($1.05 billion). All of these are owned and operated by Asian firms. PC-darling Valve continues to do well, claiming two spots among the top earners, for a combined total of almost half a billion dollars. Part of the current momentum behind Dota 2 can be attributed to its growing popularity as a competitive game and Valve's genius in crowdsourcing prize pools. Doing so has produced some of the highest tournaments winnings, attracting headlines everywhere, and offering increasing evidence that eSports is becoming commonplace.

Mobile is getting top-heavy and is up for renewal.

At first glance there doesn't seem to be a lot of fresh information among the top ranked titles: Supercell is still running the show, Machine Zone perpetuates in second position and the various Candy Crush titles continue to hold their appeal. But that's not an entirely fair assessment. In addition to the usual suspects, we now also see a few newcomers: Fantasy Westward Journey (NetEase), Colopl Rune Story (Colopl) and Disney Tsum Tsum (LINE). Collectively, these new entrants underscore the strength of the Asian mobile games market as it grew in overall importance over the past year. Individually these games present a wider variety of game companies, each with a different approach to the mobile games market, offering consumers more diversity. For the coming year, we are also already seeing several promising up-and-coming titles that may very well give Supercell a run for its money: Mobile Strike (Machine Zone), Clash of Kings (ELEX Wireless), the recent release of Westward Journey 2 (NetEase) in China, and, finally, the success of Kabam's Marvel Contest of Champions.

Outlook

Here's a principle to keep in mind as 2016 unfolds: the top game publishers are becoming so large that they can no longer sustain their growth by simply publishing more titles and claiming more market share in games. They will have to expand into other, larger markets to meet their fiduciary obligations to shareholders and focus on making their business more money. If we add the earnings of all of King's titles to Activision, we see the effect of the recent acquisition as Activision goes from $1.7 billion to $2.9 billion across digital platforms. Almost in the same breath, Activision acquired MLG to extend its efforts in competitive gaming, and hired a well-known Hollywood producer to oversee its movie ambitions. Elsewhere we see companies like Tencent, Nexon, NCSoft and others, which all hold dominating shares in their domestic markets, becoming increasingly keen on enlarging their global footprint.

In summary, 2015 has been a banner year for the games industry as digital games are now the norm. It has allowed a host of new companies to enter the market, and is forcing consolidation as the big publishers get bigger. But the real power ultimately lies with the consumer, and that is where the growth truly stems from: a greater acceptance and overall adoption of digital distribution and its accompanying monetization models.

As gaming takes its place as a full-grown member of the entertainment industry, the role of its leaders will change. It will require a broader strategy both in terms of channels and geographies, an inevitable emphasis on efficiencies across platforms as companies grow, and a greater control over the user acquisition component.