Stock Ticker: Nintendo

Six months of decline - but what do the markets actually want from Japan's one-time giant?

In the wake of Nintendo's conference last week in Tokyo, it was widely reported that the company's stock fell by around 5% in trading after the announcement of the firm's new games for the 3DS. It's a stinging reaction for a company which only a couple of years ago was valued (ridiculously) as Japan's second most valuable, after the world's top car manufacturer, Toyota - but to understand what that kind of swing means, it's important to look more closely at the stock and its recent history.

First of all, let's look at the context to the movement - specifically, the performance of Nintendo's shares over the past year. It's tempting to look further back and consider the dizzy heights of 2007's ridiculously over-enthusiastic valuation, but while that would give us an extremely steep graph to cluck about, it's not actually all that helpful or informative. Suffice it to say that if you were an investor so swept away in the excitement of the Wii and DS' market dominance three years ago that you actually bought Nintendo shares at their peak, they've now lost 80% of their value and you've probably been fired (and rightly so).

The reason that isn't really a helpful graph is because several very important things happened in the years since Nintendo's valuation peaked, and neither of them had anything to do with Nintendo itself. The first was the credit crunch - often called the "Lehman Shock" in Japan - which was responsible for the vast bulk of that loss of value. After the Lehman Shock, Nintendo's stock had dropped 60% of its peak value - so events since then only account for the last 20% of the decline.

Dismiss as nonsense any claim that the enormous decline in share value since 2007/08 is a sign that the markets think Nintendo is on a road to utter disaster.

Moreover, "events since then" also encompass the Great Touhoku Earthquake six months ago, which understandably impacted on share prices in Japan, and the historically strong Yen, which has been extremely damaging to export-led industries (including Nintendo), and has also depressed Japanese stock prices. None of that has anything to do with Nintendo's business model or product line-up, so our first order of business is to dismiss as nonsense any claim that the enormous decline in share value since 2007/08 is a sign that the markets think Nintendo is on a road to utter disaster.

The markets, let's not forget, still value Nintendo at over 1.5 trillion Yen - a far cry from their extraordinary valuation in 2007, but still the world's most valuable games company. That valuation racks up to some £12.4 billion plus spare change at the present exchange rate, which makes Nintendo almost 50% more valuable than Activision Blizzard.

What we need to look at instead, then, is share performance over the past year - an indication of how the markets think Nintendo is doing right now, free of the rapid, aggressive value correction which came about after the Lehman Shock woke everyone up to the overvaluation not just of Nintendo, but of countless other stocks as well. Here we go:

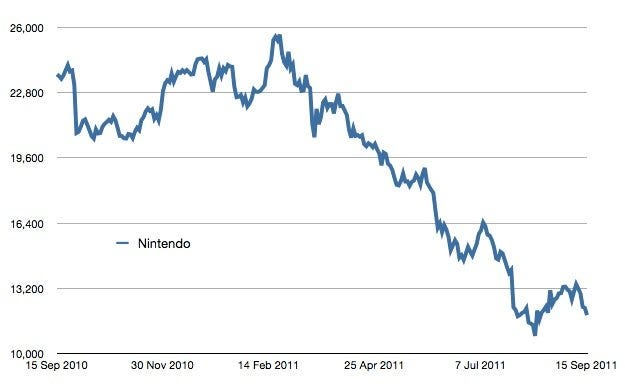

This is Nintendo's one-year chart. The overall trend is easy to see - while the first few months are bumpy, there's as much optimism as there is pessimism in the pricing, but then around mid-February, the prices start a steady decline which brings us pretty much right up to the present point in time.

Two things happened in February/March which are worth considering when looking at this graph. The first, of course, is the earthquake on March 11 - and you can see the influence of that easily, in the form of the very steep price drop in early March, which then seems to be mostly corrected out over the course of the next few weeks. The other thing, of course, is the launch of the 3DS - and at first glance, it certainly looks like Nintendo's fortunes on the stock market have been on a downward trend from exactly the point when the 3DS hit store shelves.

It's also worth pointing out that E3, which took place this year at the end of the first week of June, caused a further price slide - that's in the wake of the Wii U announcement. In fact, the slide that we saw after Nintendo's pre-Tokyo Game Show conference isn't actually particularly pronounced compared to various other precipitous falls in the company's stock value this year.

Before we look in any more detail at this chart, though, it's worth coming back to the questions of the Great Touhoku Earthquake and the incredibly strong Yen - both of which have had a major impact on Japan's economy this year. If you truly want to see what market sentiment regarding Nintendo is like, you need to correct for those factors somehow. Take a look at the next graph:

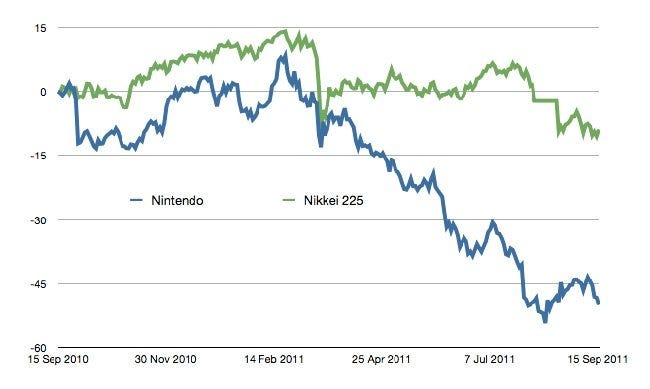

The green line in that graph is the Nikkei 225, an index which tracks the performance of most of Japan's top publicly quoted companies. By an odd quirk, Nintendo isn't actually on this index despite its size - this is because Japan actually has two stock exchanges, one in Tokyo and one in Osaka, with the Nikkei 225 being based on firms listed on the Tokyo exchange. Nintendo, a company which has been headquartered for over a century about half an hour outside Osaka in the suburbs of Kyoto, is listed on the Osaka exchange.

Despite this, however, the Nikkei 225 is a solid way to see the influence of macro-economic factors on Japanese share prices - so divergence between a company's performance and the NI225's performance is a fair measure of success or failure. On that front, this graph is extremely telling. Nintendo's shares tracked the Nikkei fairly closely up until mid-February (as you'd expect from a comparison of a single stock to a large index, the ups and downs are a bit more pronounced, but there's nothing dramatic there). Then a steady decline begins which drags Nintendo's valuation further and further south of the movements in the NI225 - with the earthquake again visible on the graph, but even more clearly a temporary rather than lasting effect.

What this means, in essence, is that even once you account for macro-economic factors, the markets aren't happy with Nintendo. There's a steady price decline visible, and worse, the points when that decline are reversed are little to do with Nintendo's own strategies. A peak in early July is matched on the Nikkei 225 index, because it's related to currency fluctuations rather than anything Nintendo itself did.

In August, Nintendo dropped to a five-year low after announcing very weak financials (by its own high standards, I should point out - the company is in absolutely no financial trouble at this point), but then started to rise again sharply. Some of this is down to the market correcting for an over-reaction, but some commentators also implied that investors were reassured by the aggressive nature of Nintendo's 3DS U-turn. The truth of that rise is rather more prosaic. The Tokyo Stock Exchange is presently in talks to take over the Osaka Stock Exchange, which would mean that Nintendo could well be listed on the NI225 index - a move which would force institutional investors to buy Nintendo stock as part of their NI225 portfolio. The potential for that change drove Nintendo's stock higher (along with several other companies on the Osaka exchange), not investor excitement around the 3DS' new price point.

In the more immediate term, it's also worth noting that Nintendo's 5% fall in the wake of their TGS conference seriously underperformed the NI225 on that day, so yes, it's fair to say that it was a direct market reaction to the conference. However, when looking at all of those things, it's important to understand what markets actually react to - because it's not the same stuff that consumers or industry insiders react to.

There are complexities to day to day behaviour, but in the long run, stock markets reward only one thing - growth potential. It's tempting to assume that a company which continues to be profitable in a steady manner will maintain a steady share price, but that's not how the markets work. If you make $100 million this year, that's great, but unless investors can see a path towards making $110 or $120 million next year, they'll desert you in droves. Investors in the stock market are looking for strong growth - if they wanted low-risk and low-yield, they'd be investing elsewhere (government bonds, for example). Nintendo's immense share price a few years ago was down to the fact that it was growing its market at a rapid pace - its decline now isn't necessarily reflective of a huge decline in market share, but rather of the fact that investors have lost confidence in the company's ability to keep growing.

The markets aren't punishing Nintendo because they think it won't be profitable in future - they're punishing it because they think it can't return to the stellar growth of the Wii era.

Specifics, oddly, don't matter that much. Industry insiders and commentators can look at deals like the one which is bringing Monster Hunter to the 3DS and understand that this is an important release that will do great things for the console's uptake in certain markets, but on the whole, the markets don't care about that. Sentiment around Nintendo is negative at the moment, because investors see the company's last console release as a failure and worry about its market being eaten up by mobile phones (both reasonable positions to take). That sentiment overpowers any detail within the picture - until Nintendo can come up with something that incredibly clearly demonstrates its ability to triumph over devices like the iPod Touch, the markets are going to keep avoiding it.

Does that mean, as some people have suggested, that the markets want Nintendo to abandon hardware manufacture and focus instead on developing games for mobile devices? Absolutely not - and those who argue in favour of that are largely just confirming their own biases with market data, rather than considering the wider picture.

Nintendo makes a huge amount of money from hardware sales; even if the new price point for 3DS means that it's selling at a small loss right now, economies of scale will soon fix that. To begin publishing on mobile devices would effectively mean debasing its own hardware platforms - it would still have to support its own hardware for some time (or risk losing massive amounts of goodwill from its consumers) but would be doing so expensively, in the face of diminishing sales. Meanwhile decommissioning the hardware business and transitioning the company to mobile would also cost vast amounts of cash - and at the end of this painful, expensive process, there's no guarantee that third party mobile publishing could ever match Nintendo's former revenues from hardware and software.

What the markets hate most of all is uncertainty (note that after Steve Jobs' resignation, Apple's stock price actually rose, because it ended the speculation and uncertainty over the company's future administration), and that path is filled with absolutely nothing but uncertainty. That isn't to say that from a business perspective, it isn't the right thing to do - but while a smarter, leaner Nintendo focusing on titles for other publishers' platforms makes sense to those of us following the industry closely, it's a massive stretch to suggest that the markets are "calling" for Nintendo to do that. On the contrary - it would make such a transition at risk of completely destroying the value of its own shares, at least in the short to medium term.

Are the markets happy with Nintendo right now? No. Is the company's stock price likely to improve in the short term? No, not really. It's likely to continue a gentle decline before finding a fairly sensible base price that reflects the company's true prospects. Is this, however, a sign that Nintendo is "doomed"? Absolutely not. The firm faces huge challenges, but its cash position is fantastic and it's still got enormous sales and market share. The markets aren't punishing Nintendo because they think it won't be profitable in future - they're punishing it because they think it can't return to the stellar growth of the Wii era. On that front, they're almost certainly correct.

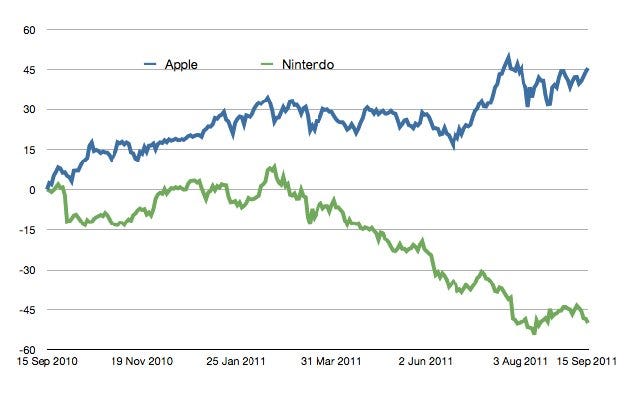

To close, one more graph of stock performance over the past 12 months. A disclaimer; this is an entirely unfair comparison of two companies with very different business strategies and product line-ups - but by accident or design, they're the two companies who are the chief cheerleaders for the traditional packaged goods and the app store distribution models respectively. Whether they like it or not, these two giants are going to spend the coming years at each other's throats - and it's fairly clear which of them is winning in the first round.